A week ago, we guaranteed a more point by point clarification of our present market sees. We need to focus this week on securities, where honestly we trust value activity bodes well than in value markets. To set the scene, we are emphatically arranged to US bonds particularly contrasted with center European bonds which we keep on believing offer to a great degree poor esteem. With no new evident wellspring of development and poor socioeconomics, record large amounts of obligation all over and wide and additionally compounding disparity in numerous Western nations, the world economy stays in the "wade through" stage, best case scenario. Indeed, considering the develop period of the financial cycle, combined with worldwide fiscal strategy creators now fixing money related approach, we trust that there are openings in some top notch settled pay zones. This all needs some further clarification, so we should make a plunge.

To start with, we appear in outline 1 beneath the historical backdrop of the US 2s10s yield bend, the parts of this emphasis of the yield bend and the Government Assets target rate. On the off chance that we begin by taking a gander at the Fed Assets rate (in blue), unmistakably as the Fed raises and diminishes financing costs, the 2 year security yield extensively takes after. This bodes well. Nonetheless, the Fed has less control over longer dated securities which are influenced by elements like swelling desires, term premium and in addition the normal way of short rates later on.

As can be seen obviously in measuring the contrast between the yields on the 2 and 10 year security (the green line in the lower board), there can be some extensive swings after some time. Generally, zero or a bit beneath is the lower limit and in the vicinity of 300bps is the upper limit. As we as a whole know, the post Extraordinary Budgetary Emergency (GFC) recuperation has been similar to no other in a few regards, particularly when taking a gander at US financial strategy. With QE intended to takeover from loan costs in fortifying the economy, scholastics outlined a shadow Sustained Assets rate to quantify this additional convenience. We have noted with the white vertical lines the date that this purported shadow Bolstered Assets Rate bottomed at about less - 3%. We can contend later whether the Federal Reserve's fixing cycle begun at the low of the shadow rate in May 2014, or the top notch ascend in December 2015, however what is evident today is that the Federal Reserve is fixing strategy, which is prompting a narrowing between the yields on 2 year and 10 year securities; a leveling of the yield bend.

Graph 1 – US 2s10s bend with Nourished Assets rate

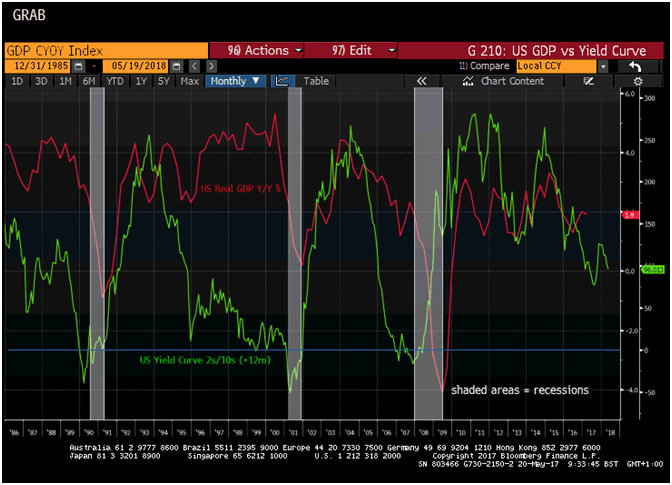

The reason the above diagram is so vital is suggested in graph 2 underneath, which demonstrates the US 2s10s yield bend (in green) and US genuine Gross domestic product year on year (in red) with retreats appeared by the shaded ranges. We have propelled the yield bend by 12 months. There is nobody single marker that has a faultless reputation in determining US retreats, however in the event that we were marooned on a leave island and offered just a single pointer, we would pick the yield bend. As can be seen, the last three subsidences were gone before by the bend rearranging (10 year yields exchanging at under 2 year yields).

For what it's worth, developments in the yield bend are not that terrible a pointer of future changes in US development, with the late 1990s time frame being a conspicuous special case when the smoothing yield bend won for quite a while as the economy performed firmly. We would propose this is the peculiarity. In the late 1990s, the web prompted a small scale (at the end of the day impermanent) surge in efficiency. As noted above, we are attempting to perceive any new wellsprings of development in the following couple of years, other than a monetary spend lavishly that appears to be more outlandish today than it did the day after the US decision last November.

Outline 2 – US 2s10s yield bend and genuine US Gross domestic product development Y/Y %

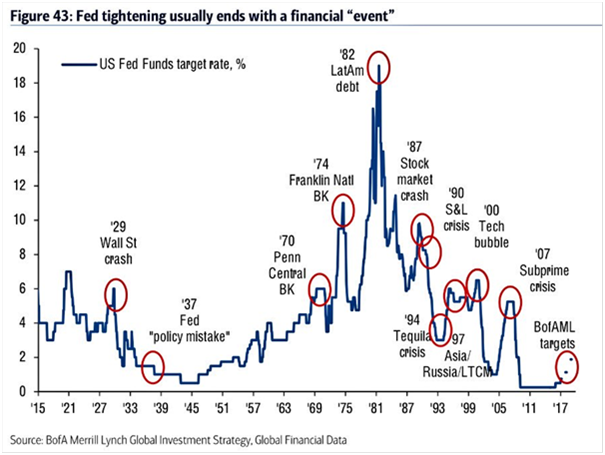

Thus, without going into a profound plunge on the present and planned execution of the US economy, our straightforward guide is that the Federal Reserve is raising rates, and dissimilar to a year ago, appears to be determined to doing as such (and conceivably decreasing its accounting report) paying little respect to the execution of the genuine economy – the Q1 miss is being expelled as short lived by Sustained individuals. As demonstrated by the Bank of America Merrill Lynch diagram we indicate again underneath, once the Fed begins a fixing cycle, they proceed until something breaks, either at home or abroad. We trust that the Fed will keep fixing strategy until something breaks, and this will be clear by a further straightening of the yield bend as the 2 year security yield rises however the 10 year security yield stays enduring or even drops if recessionary signs increment.

Outline 3 – The historical backdrop of Nourished fixing cycles finishing seriously

We nitty gritty a few times amid late Q1 how we were glad to incline toward the "reflation" story that was well known in the business sectors at the time. We were cheerful to express this view by owning US 10 year securities by means of the prospects showcase, and have stayed since a long time ago close to the lows in Spring. In any case, regardless of the possibility that we are correct that the yield bend levels in the months ahead, this can happen with 10 year yields slashing around sideways or moving lower. We have delighted in a decent little keep running in our settled salary positions and we have started to take benefits as we stress that cost might be entering a transient combination stage – to be clear, we will be decreasing our introduction as a strategic change because of market valuing and situating as it were.

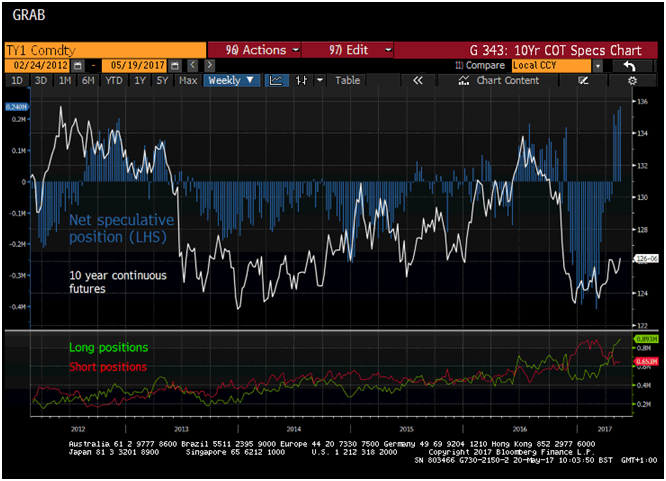

Diagram 4 shows the 10 year Treasury Fates cost nearby theoretical situating.

What concerns us at this moment is that theorists have moved from being record net short in bonds to the longest net position since the GFC. To take a gander at the circumstance at a more granular level, that move in net situating has happened as long positions (green line in bring down board) have detonated higher. Yes, short positions remain very lifted, and further covering of those positions could push costs higher, however with a close record long position now held, there must be space for some long position liquidation if monetary information makes strides. We are subsequently taking a few benefits as we would prefer not to get gotten on the wrong side of a brief crush on long positions.

Outline 4 – US 10 Year Treasury and theoretical situating

Widening out the talk here, and as said toward the starting, we keep on believing that center European bonds offer no an incentive to speculators today. Long-term perusers will recall that we railed against the negative yielding securities the previous Summer, and albeit longer dated securities now offer a positive yield, shorter dated securities don't. This can just keep going inasmuch as the ECB is seeking after both QE and negative store rates, in any case, as clarified a week ago, the European National Bank has all the earmarks of being moving far from these outrageous strategies.

With month to month resource buys down from EUR80 billion to EUR60 billion, the ECB has just dedicated to keep up this pace until year end. Some in the market trust that the ECB will refresh their arrangements for one year from now at their June meeting, nonetheless, we speculate that they will hold up until September. What is clear is that without another emergency or diving expansion, the ECB will be diminishing QE encourage one year from now. We likewise presume that they are quick to raise the store rate from the present less - 40bps back to zero when for all intents and purposes conceivable. It is critical to comprehend that even among focal managing an account elites, there is no acknowledged intelligence that negative rates are either viable nor attractive over the more extended term. What's more, on this note, improvements late Friday, with reports that Merkel needs Jens Weidmann to assume control from Mario Draghi when he ventures down in late 2019, may well add to the weight for normalizing rates one year from now.

Anyway, expecting we are correct that center European yields are just exchanging negative domain today in light of QE and negative rates conveyed by the ECB, at that point would we say we are on the whole correct to accept that these security yields will move into positive landscape as the ECB exits these outrageous arrangements? We suspect as much, and we think the procedure granulates on throughout the following 12 months and the sky is the limit from there. We likewise think an exquisite approach to endeavor to benefit from this pattern is to short 5 year German bonds as opposed to being long 5 year US Treasuries.

Outline 5 demonstrates the connection between the two.

Specifically, the green line in the lower board measures the yield distinction amongst US and German 5 year security yields, and as can be seen the hop higher post the Trump triumph pushed the distinction to a verifiably wide level. So the question here is basic. There gives off an impression of being a flexible band between these two that infers that the distinction can't stay over 200 premise focuses for that long. Assuming this is the case, what future results will make the distinction limit or augment?

Outline 5 – US 5 year yield versus German 5 year yield

Maybe the primary indicate make here is the undeniable one. On the off chance that nothing happens and yields just continue as before, at that point our long US versus short Germany will pay us over 2% for each annum which is a pleasant convey exchange a close to zero rate world. As noted, we are accepting that German yields can't move much lower and regardless of the possibility that the ECB at last needs to accomplish more, German yields can't move much lower than the current lows of short 60 premise focuses. We along these lines contend that the drawback from the German leg of our exchange is around 25 premise focuses. We would likewise accept that an occasion that caused the ECB to go full scale again would be sufficient for the Fed to quit fixing arrangement, and maybe even begin cutting rates (how about we not overlook that few FOMC individuals continue revealing to us that they may need to accomplish more QE amid the following retreat).

So the hazard in our exchange is that US yields rise more quickly than German yields. Furthermore, despite the fact that this is impeccably conceivable, as we have noticed, our conviction is that the Fed will fix strategy until something breaks, which for the 5 year part of the bend implies that any important ascent in yields because of Bolstered arrangement will probably be either overlooked by the market as the yield bend smoothes or immediately turned around as the Fed handles the emergency that they make. Meanwhile, if no reflation of emptying occasion unfolds, we will gather our 2%+ convey.

Obviously, there are no certifications and unquestionably no free snacks in money related markets, yet we do imagine that this exchange can work in both a gently "hazard on" condition (as observed so far this year amid which time the yield spread has limited from around 245bps to 215bps), and in a "hazard off" condition as the Fed inverts course. The condition that damages this exchange is a one-sided reflationary condition in the US, which was unmistakably the underlying business sector response when Trump was chosen (and the spread hopped from 170bps to 260bps in short request). As we have clarified a few times since the Trump triumph, we don't see the US reflation exchange as a practical result; surely not to the extent that could cause the yield spread to hole by an indistinguishable sum from last November/December.

On the off chance that Trump can recover his development strategy motivation on track, we speculate that the yield spread would extend however at a more unobtrusive pace. Nonetheless, our unique questions of the capacity of Trump to convey an important development motivation have just been reinforced by his execution since he took office.

So once more, perceiving there are no free snacks, we truly do like the look of the long US 5 year versus short German 5 year exchange, as it pays an exceptionally pleasant convey for basically holding the exchange. We have not been harmed by the exchange amid the value advertise expansion seen since February and we would expect an exceptionally positive return if markets move to a hazard off period which would most likely lead the Fed to downsize on their money related fixing process.

So to wrap up our security showcase considering, we are humbly long US 10 year securities as we see the Fed on a fixing way until something breaks, which would most likely at that point drive security yields lower. We anticipate that the yield bend will keep on flattening in the months ahead too. On a relative esteem premise, we are long US 5 year bonds versus short 5 year German bonds. Actually, this is our single greatest exchange our multi resource full scale finance.

One week from now, we will really expound on our value advertise contemplations and current exchange thoughts. As we have point by point finally, the principal setting is that long haul value returns are probably going to be poor since value markets have risen such a great amount since 2009 and valuations are costly, particularly so in the US. In any case, valuations don't drive here and now showcase execution; financial specialist assumption does. We have been sitting tight quietly for signs that conclusion towards US values is going to change, and the present market setup is amazingly intriguing to us.

As noted above, we have been taking a few benefits from our US security property, and we have taken those benefits (and a touch of additional capital) and put that into bearish choice techniques. We will analyze these in more profundity one week from now, yet with a greatest pay out of 7.3:1 from these choices, and our misfortune restricted to the premium paid, we trust that our potential reward in the event that we are correct is great contrasted with the capital we are gambling. We even got a little energized when US values sold off mid-week as Trump's inconveniences raised, in spite of the fact that the ricochet into the end of the week was clearly baffling. We will broadly expound on this one week from now.

upvote me i am doing that for you

its a very informative topic ,a best piece of information you really deserve for upvoting on that post keep it up my bro nice work cheers i am supporting to you its a very helpful topic following you my bro