Why Bitcoin Still Needs Fiat (And This Won't Change in 2018)

!

Tim Swanson is the director of research at Post Oak Labs, a U.S.-based technology advisory firm, and the former director of research at distributed ledger technology consortium R3.

The following article is an exclusive contribution to CoinDesk's 2017 in Review series.

Imagine a parallel universe in which the U.S. economy could only grow at $50 every 10 minutes generating a mere $2.6 million of output per annum. That due to a hard-coded economic planning computer program, every four years the income its inhabitants collectively generated divided in half. Such that in year nine, its output shrank and was $12.50 every 10 minutes or $657,000 a year.

That is to say, irrespective of how productive and skilled the labor force became or how large the labor force grew, the productive output in the U.S remained fixed and static with the only change (downward in this case) occurring just once every four years.

How many people would volunteer to live and work in that "Upside Down" world?

This situation effectively mirrors the static, internal economy of bitcoin and many other cryptocurrencies.

For instance, with proof-of-work networks like bitcoin, the marginal productivity of labor is zero. It does not matter how many more units of labor are added to the income generation (mining) process as the network will always produce the same amount of economic output.

Today, after nearly nine years of operation, the bitcoin network – better referred to as Bitcoinland – generates 12.5 bitcoins roughly every 10 minutes. Irrespective of external economic conditions, of demand, the Bitcoinland economy will generate about 657,000 bitcoins per year in its third epoch.

While comparisons with aggregate measurements like GDP and money supplies may be an imperfect analogy, the fact that economic expansion as measured in output can – with the exception of a fork and rule change – never change in bitcoin due to its inelastic coin supply is arguably detrimental to its unit of account.

The purposefully planned sameness is often extolled as a "feature not a bug," and many cryptocurrency enthusiasts like to daydream for when regulators and financial institutions of our own world disappear, eaten up by grey goo nanites funded by bitcoins.

But before bitcoiners can reach their Upside Down nirvana state, they need to resolve the underlying omnipresent economic calculation challenge facing their security system and labor force.

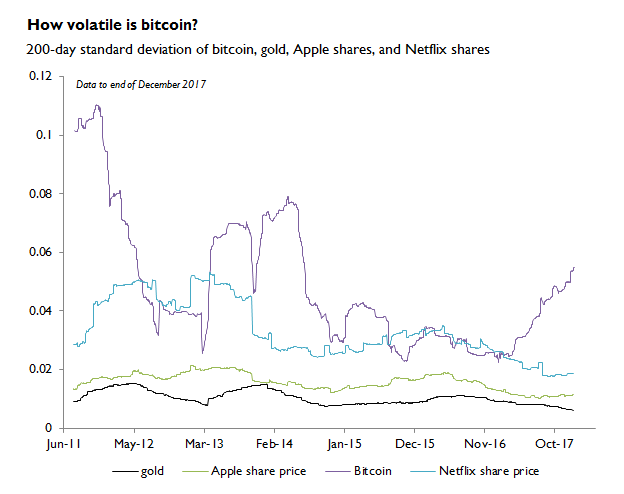

The phenomenon is simple to describe: virtually no participant in Bitcoinland conducts economic calculations (such as pricing) for any goods or services in cryptocurrencies such as bitcoin. There are many reasons for this, including chronic volatility.

Courtesy of J.P. Koning

Or increasingly high ($10+) transaction fees that result in hemorrhaging of merchants (even their very own Cobra Commander acknowledges this issue).

But for this article, let's put aside the typical discussion of payments and merchants and instead focus on labor.

Labor force

If Bitcoinland is viewed as its own sovereign (virtual) nation-state, the only wages any native participant receives in return for any kind of service rendered is what miners are paid to solve and "vote" on a benign problem about once every 10 minutes.

From the perspective of the network: developers, maintainers, administrators, enthusiasts, Twitter sock puppets, meme artisans, flame war veterans, self-appointed thought leaders, pumpers, hat wearers, etc., are all viewed as foreign third parties and can only receive bitcoins after they are first minted by the miners.

Much like multinational corporations (MNC) with large overseas operations, miners of cryptocurrency networks as a whole do not measure the income they receive in terms of bitcoins (or other discrete cryptocurrencies), but instead they measure their income in terms of "fiat" from foreign financial markets, specifically converting bitcoins into the local fiat currency where their mining operation physically resides.

However, unlike MNCs that eventually repatriate some or all of their capital back to their headquarters, aside from a recycling of coins into ICOs, most cryptocurrency-focused companies are still dependent on what amounts to foreign domestic income (FDI), regular injections of foreign capital from venture firms in order to grow or even measure enterprise valuations.

Miners do this because the unit of account for fiat currency is typically stable and liquid, such that they can pay wages to their employees, pay rent, electrical costs, property taxes, etc. There are exceptions to stability, such as planned economies of Venezuela and Zimbabwe which have suffered from years of political chaos, but in general, most developed countries and even developing countries have relatively stable domestic currencies relative to Bitcoinland.

And because bitcoin is still not used as a unit of account, its labor force (miners), rely on a third-party reference data in order to conduct all economic calculations. That is to say, in order for Bob the miner to accurately calculate if he should increase or decrease consumption (and investment) of capital, or to measure whether his mining operation is profitable, Bob projects future revenue based on a unit of account that is stable, in this case, currency from foreign capital markets.

During the Cold War there was a joke in academia: that the Soviet Union would conquer the world with the exception of New Zealand (other versions used Switzerland as the cut-out). New Zealand would be left alone because the Politburo needed a functioning market so that the Soviets could know what the market prices were for goods and services.

While Bitcoinland may be attracting large sums of foreign capital, miners continually still need very liquid over-the-counter (OTC) and spot exchanges denominated in foreign currencies because it is with these foreign currencies that they pay their bills.

In this case, despite their own defects and problems, the U.S., eurozone, Japan, South Korea, China and several other countries effectively stand in for "New Zealand," such that the national currencies and prices in these countries reflect dynamic economic conditions that bitcoin miners can use as reference rates in their capital consumption projections.

Final remarks

In 2018, just as the past nine years, miners will still depend on foreign financial markets for both stable pricing and liquidity. If the existing traditional financial markets became chaotic and unstable, miners would be unable to rationally plan and allocate for future investments.

For instance, the unseen costs of hash generation for a hypothetically stable $20,000 bitcoin would be about $13 billion in capital consumed by miners in their rent-seeking race.

And that is just one proof-of-work coin. If there were dramatic bouts of volatility, or even an extended bear market, this could result in bankruptcies like CoinTerra, HashFast or KnC previously went through, though that is beyond the speculation of this article.

Ironically, despite all the bluster, because cryptocurrency ecosystems lack a circular flow of income, they will still be dependent on the very financial system they vilify for daily support and stability.

And while there have been many "stablecoin" projects announced and launched over the past year, nearly all of them are not only dependent on commercial bank accounts, but also on the economic stability of a specific economic region they aim to serve. Guess what set of entities provides that type of relative stability?

Ideological enthusiasts will likely resort to whataboutisms and respond by bitcoinsplaining: how dirty filthy statists will censor your virtuous darknet market transactions and that maintaining proof-of-work networks is worth any cost to the environment! But again, that is for a snarky article on a different day.

Empirically with proof-of-work-based blockchains, the labor force and the liquidity providers all still depend on functional, mature foreign capital markets in order to convert their coins into real money. Perhaps this will change as more hedging products, courtesy again of foreign financial markets, are brought online.

While the traditional financial markets will continue to exist and grow without having to rely on cryptocurrencies for rationally pricing domestic economic activity, in 2018, as in years prior, Bitcoinland is still fully dependent on the stability of foreign economies providing liquidity and pricing data to the endogenous labor force of bitcoin.

Too much macroeconomics for you? CoinDesk is accepting submissions for its 2017 in Review series. Email news@coindesk.com to tell us your thoughts on the year ahead.

Upside Down world image via "Stranger Things" Facebook page

The leader in blockchain news, CoinDesk strives to offer an open platform for dialogue and discussion on all things blockchain by encouraging contributed articles. As such, the opinions expressed in this article are the author's own and do not necessarily reflect the view of CoinDesk.

SOURCE: CoinDesk / Tim Swanson /

Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:

https://www.coindesk.com/bitcoin-still-needs-fiat-currency-wont-change-2018/